Private markets investing has undergone several evolutions over the past decades, adjusting to developments in the macroeconomic and business landscape. However, the way investors have accessed private markets investments has remained largely unchanged.

The traditional closed-end fund, a structure popularized in the 1980s, still represents the majority of the industry’s assets under management (AUM). While these structures have served institutional investors well, the same cannot be said about retail investors and the private wealth segment.

Such individual investors are responsible for only 16% of alternative investments, despite controlling half of total global AUM. 1 Furthermore, within their overall allocations, just a 5-6% 2 share is dedicated to private markets – compared to 24% 3 for institutional investors. This imbalance has fuelled a growing demand for a type of structure that better serves individual investors – the "evergreen", or "open-end", fund structure.

Evergreens work as perpetual capital funds, where investors can subscribe into and redeem out of over time, without otherwise having to wait for the vehicle's termination. The liquidity feature of this structure, as well as the typically lower minimum investment requirement, better caters for the needs of individual investors. (See section 3 for differences between closed-end and evergreen structures.)

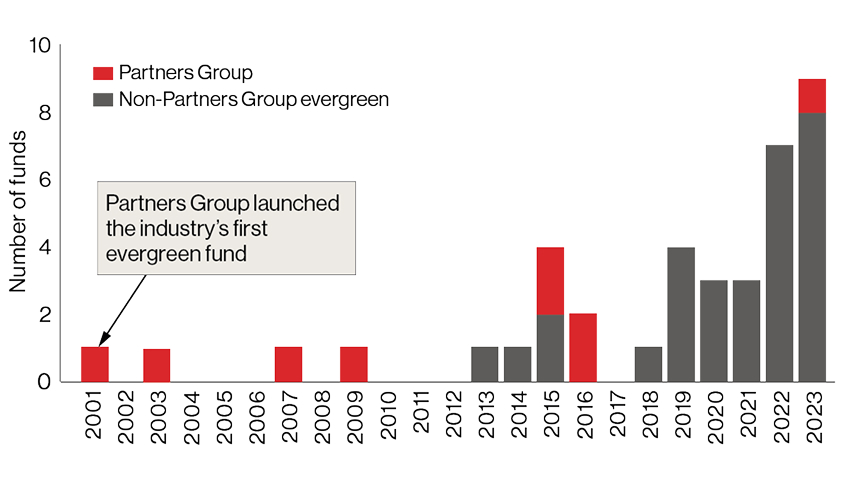

Partners Group pioneered evergreen funds more than 20 years ago, and we are a firm believer in their potential to democratize private markets. In recent years, several other market participants have started echoing this viewpoint, resulting in a record number of new evergreen funds launched. In most cases, these funds represent each manager's first foray into this space, making it difficult for investors to assess their ability to successfully run such offerings.

Evergreen fund launches globally

Note: Includes Private Equity and Private Markets evergreen funds launched since 2000. Source: Partners Group research (2024). For illustrative purposes only.

In this third paper of our Private Markets MythBusters Series, we use our experience to highlight the factors we believe make a successful evergreen fund – capable of delivering attractive returns over the long-term.

By doing this we seek to dismiss the misconception that these structures can be simple adaptations of traditional closed-end strategies. In reality, a successful manager in closed-end funds may not be able to replicate such results in the evergreen space. Most importantly, we intend to equip investors with a playbook that can help them successfully conduct their due diligence and hold managers accountable for their processes and performance.

Looking under the hood

Our approach to assess today's expanding evergreen universe is based on all our learnings over time in the space. In this paper, we break them down into five key elements that we believe make a successful evergreen fund and explain how investors can assess a manager's ability to deliver on them.