- Recent US policy shifts have intensified market volatility and global fragmentation, reinforcing a ‘brave new world’ investment thesis. The outlook comprises two distinct phases, with significant differences between the near- and longer-term perspectives.

- In the near term, tariff policies are expected to dampen growth, particularly in the US. Although the base case is for tariffs to ultimately land much lower than ‘Liberation Day’ announcements, the path remains uncertain.

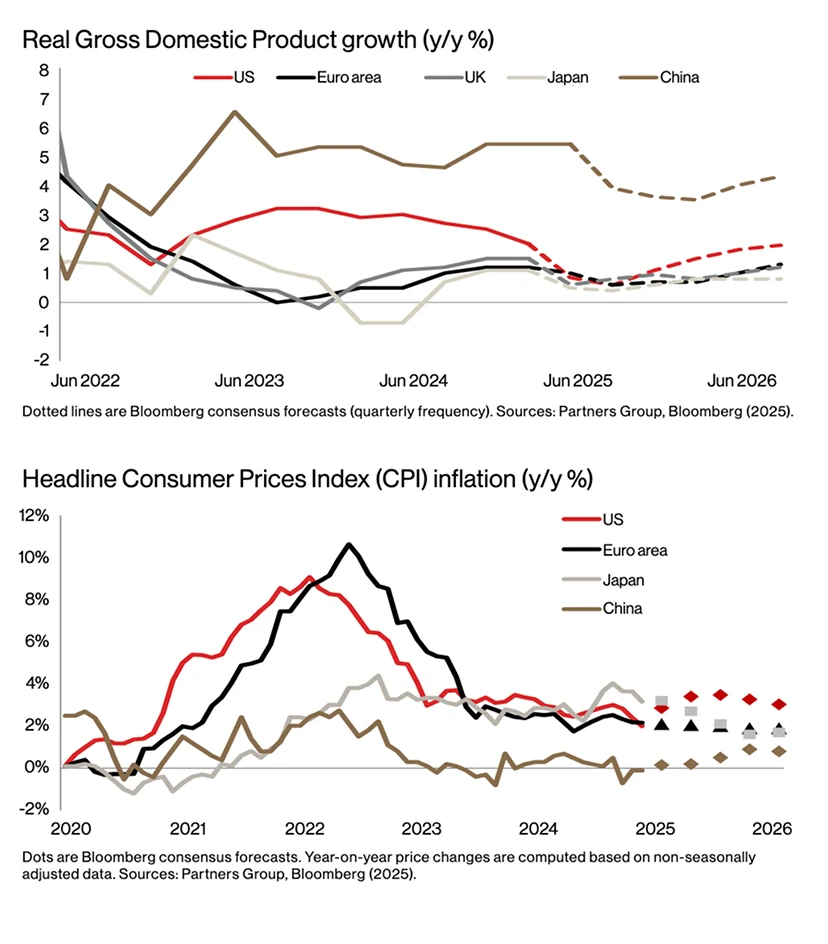

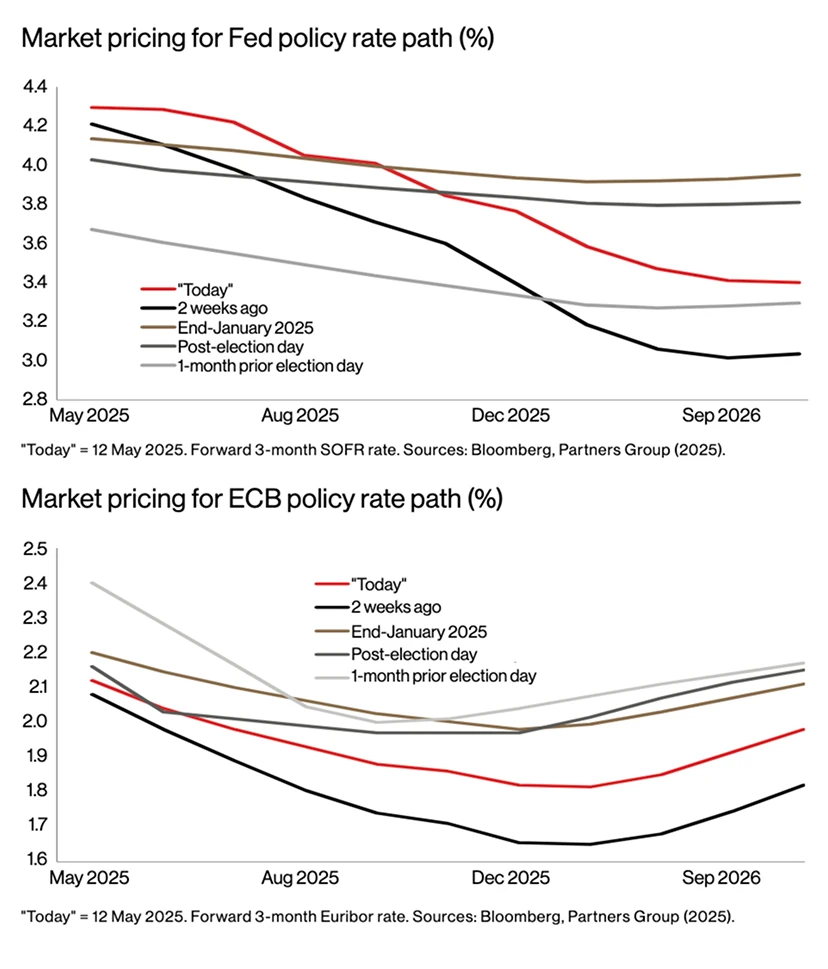

- Economic divergence between the US and Europe will persist. After recent US economic resilience, this divergence is expected to widen, particularly in near-term inflation and central bank policy. While inflation pressures are seen in the US, Europe’s disinflation trend should continue, allowing the ECB more room for monetary easing versus the Fed.

- The longer-term outlook for the US appears more positive from H2 2026 onwards, supported by policy clarity, tax cuts, and deregulation. Europe, particularly Germany, also shows promise through revised fiscal approaches.

- Private markets have demonstrated resilience, with secondaries offering opportunities amid liquidity constraints, infrastructure benefiting from inflation-linked revenues, and private credit gaining from higher base rates, while default rates remain contained.

- Despite headwinds in private equity direct transactions, investors skilled at navigating uncertainty can maximize emerging opportunities. Greater clarity on tariffs could spur an uptick in private markets activity in the second half of the year.

- This fragmented global landscape creates significant investment opportunities in onshoring and ‘friendshoring’ initiatives, though investors must navigate complex regulatory environments.

Introduction

Since coming into office just a few months ago, the new US administration has fundamentally reshaped the global economic landscape. Its policy shifts – from geopolitical realignments to the ‘Liberation Day’ tariffs – underscore our previously articulated thesis of a ‘brave new world’ of investing. This marks the end of an economic regime of macro moderation and expanding globalization, replaced by market volatility, higher interest rates, and global fragmentation.

Against this backdrop of rapid change, our midyear Private Markets Outlook offers two critical perspectives. First, we examine the immediate landscape, where recent developments have disrupted market dynamics. Second, we extend our view to assess the long-term structural shifts that will ultimately determine investment success. We conclude by examining the implications for private markets, with the aim to provide investors with tactical guidance for navigating the current turbulence and strategic vision for making the most of the transforming landscape.