Markets have priced out around 15 bps of rate cuts in the U.S. for 2026 and are now assigning a non-zero probability of rate hikes in Europe8. Despite this, we do not believe the current commodity shock is sufficient to alter central bank policy paths. Oil price shocks tend to have a limited and short lived impact on core inflation, particularly given that the U.S. and Europe are structurally less oil intensive than in past decades.

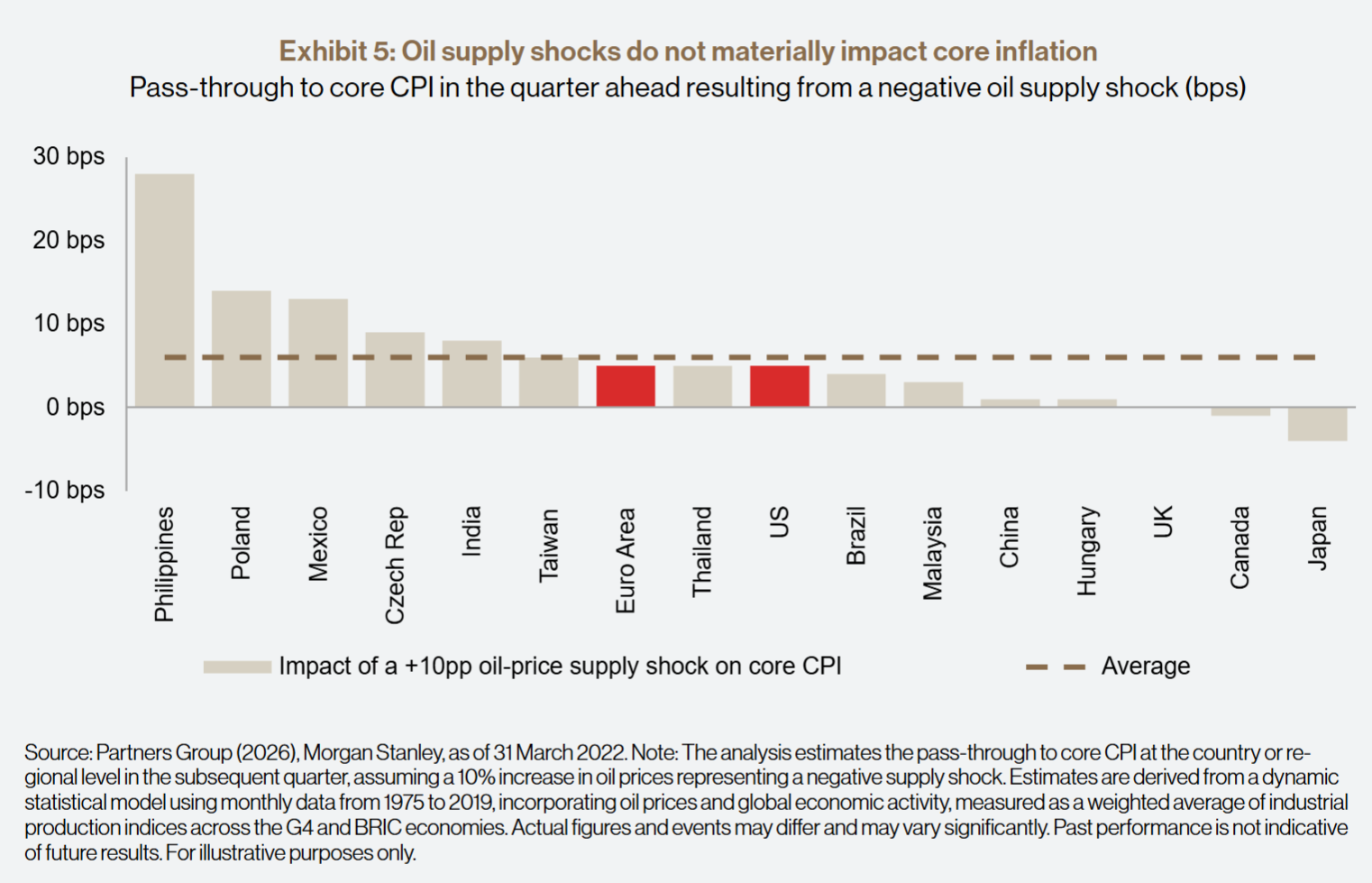

Today, a 10% increase in oil prices leading to a supply shock would, all else equal, lift core CPI across the U.S. and Europe by roughly 5 bps over the following quarter (Exhibit 5)9. In other words, the bar for oil prices to materially shift the policy trajectory is high. While policymakers dialogue and tone may shift at the margin, we believe it would require a sustained surge in energy prices – one where inflation expectations become unanchored – before policymakers would be unable to look through the move. For now, market-based inflation expectations remain broadly anchored at around 2%, consistent with central bank targets.10

The more meaningful risk, in our view, would be through consumer sentiment and the potential knock-on effect that may have on consumption, should higher energy prices persist. In such a scenario, energy costs would act as a “consumption tax,” weighing on growth and ultimately arguing for more easing, not less.

That said, under our base case, our rate expectations remain unchanged. For the Fed, we continue to expect 50 bps of rate cuts in 2026. For the ECB, we see scope for 0-25 bps of cuts in 2026, with our view adjusted modestly from earlier expectations, reflecting improved growth momentum from German fiscal stimulus rather than developments related to the Middle East.

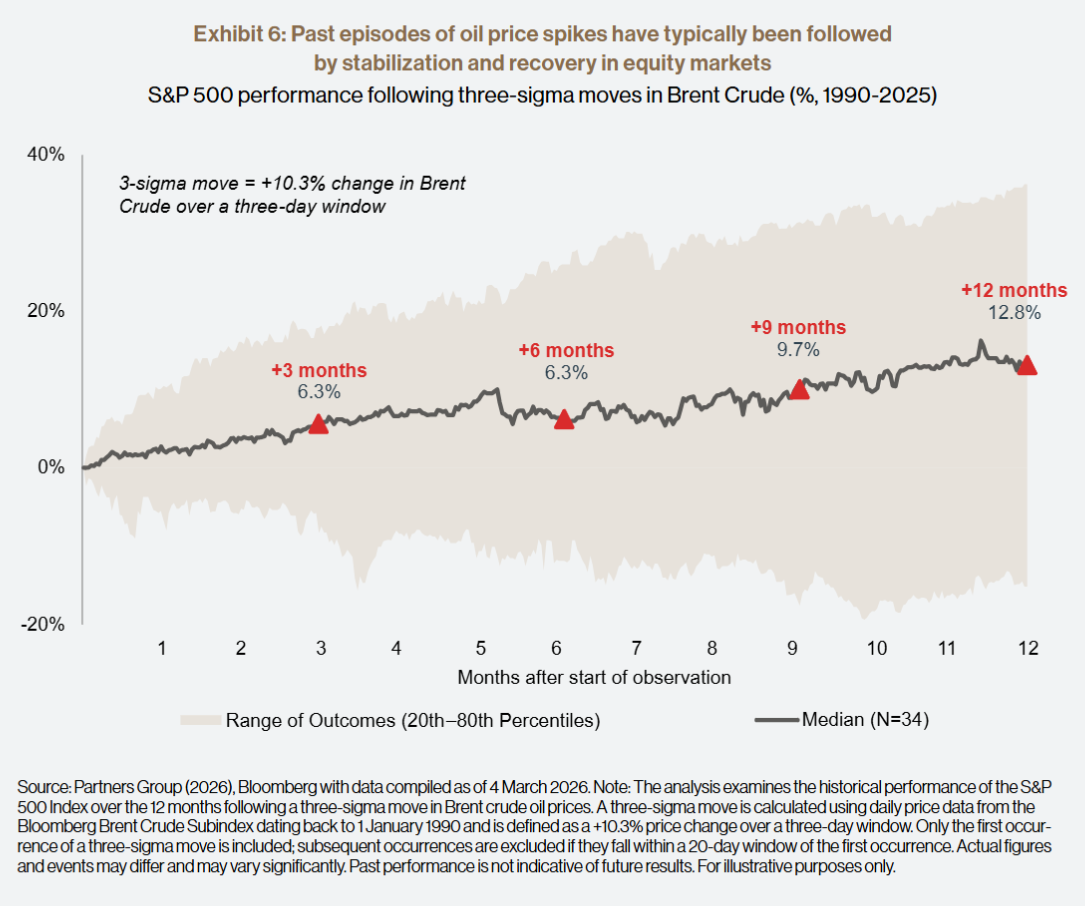

Looking beyond near term volatility, history suggests that markets tend to look through geopolitical driven energy shocks. Past episodes of sizable11 oil price moves have typically been followed by stabilization and recovery in equity markets over subsequent months. Indeed, the median returns for the S&P 500 over the subsequent one- and three-month periods have both been positive (Exhibit 6)12.

Taken together, recent developments reinforce our view that near term uncertainty does not derail the broader macro backdrop or our long-term investment themes, and that disciplined, forward looking positioning remains appropriate.