- Global growth proved resilient in 2025, but 2026 begins at elevated market levels. ‘Investing at High Altitude’ means navigating markets near their peaks – this calls for a disciplined valuation approach and readiness for volatility.

- Policy support remains central in 2026, with US fiscal measures, European monetary easing, and China’s domestic initiatives anticipated to underpin growth and market sentiment.

- Over a longer-term horizon, transformative forces – AI, demographic shifts, evolving supply chains, and infrastructure upgrades – will shape private markets opportunities.

- Private equity activity is rebounding as transaction volumes recover and pricing remains attractive. We see compelling opportunities in control investments and select secondaries across regions.

- Private credit returns are moderating as base rates decline, but Europe offers relative value. Selective middlemarket lending remains preferred.

- Infrastructure is a strategic overweight for inflation protection and secular growth. We like mid-market secondaries and see compelling direct opportunities in areas such as US power and energy assets.

- Real estate strategy centers on vertical depth and regional selectivity. Secondaries offer compelling entry points, particularly as direct transaction activity remains subdued.

- Royalties are gaining traction as a portfolio diversifier, expanding across established and emerging sectors.

What "Investing at High Altitude" means for private markets

Key Takeaways

Overview

Global growth demonstrated remarkable resilience in 2025, sustaining momentum despite persistent policy challenges and geopolitical tensions. The backdrop for 2026, however, is different. Markets remain near historic highs, while concerns have emerged around elevated valuations – particularly in AI-related businesses – alongside uneven consumer dynamics and the growing role of non-bank financing.

We recognize these concerns and the volatility that often accompanies market peaks. Our investment approach emphasizes disciplined valuation and scenario analysis. Should volatility return in 2026, we are prepared to seize the opportunities it brings. At the same time, as global investors headquartered in Zug, surrounded by the Swiss Alps, we know that what looks like a summit today may only be the pre-Alps – the foothills before the true peaks. Higher highs may still lie ahead.

What could sustain progress toward new highs in 2026?

Policy (once again) is likely to take center stage, supporting economic growth. In the US, fiscal measures tied to the midterm elections may boost consumer confidence. Europe may see more monetary easing amid weak consumption, while China’s focus on quality of life and addressing overcapacity should support its economy. Combined with anticipated rate cuts in the US, these factors support our outlook for a rebound in private markets activity – both investments and exits – as highlighted in our recent Q4 2025 Private Market Chartbook.

Looking further ahead, the next five years may bring business cycle swings, AI-driven transformation and disruption, as well as geopolitical tensions, demographic shifts, and investment upgrade megacycles. In this 2026 outlook, we review our expectations for the year ahead, explore key forces shaping our long-term approach, and provide a relative value perspective across private markets asset classes.

![]()

Regional Outlook

US: Rate and tax cuts to support the economy into midterm election year

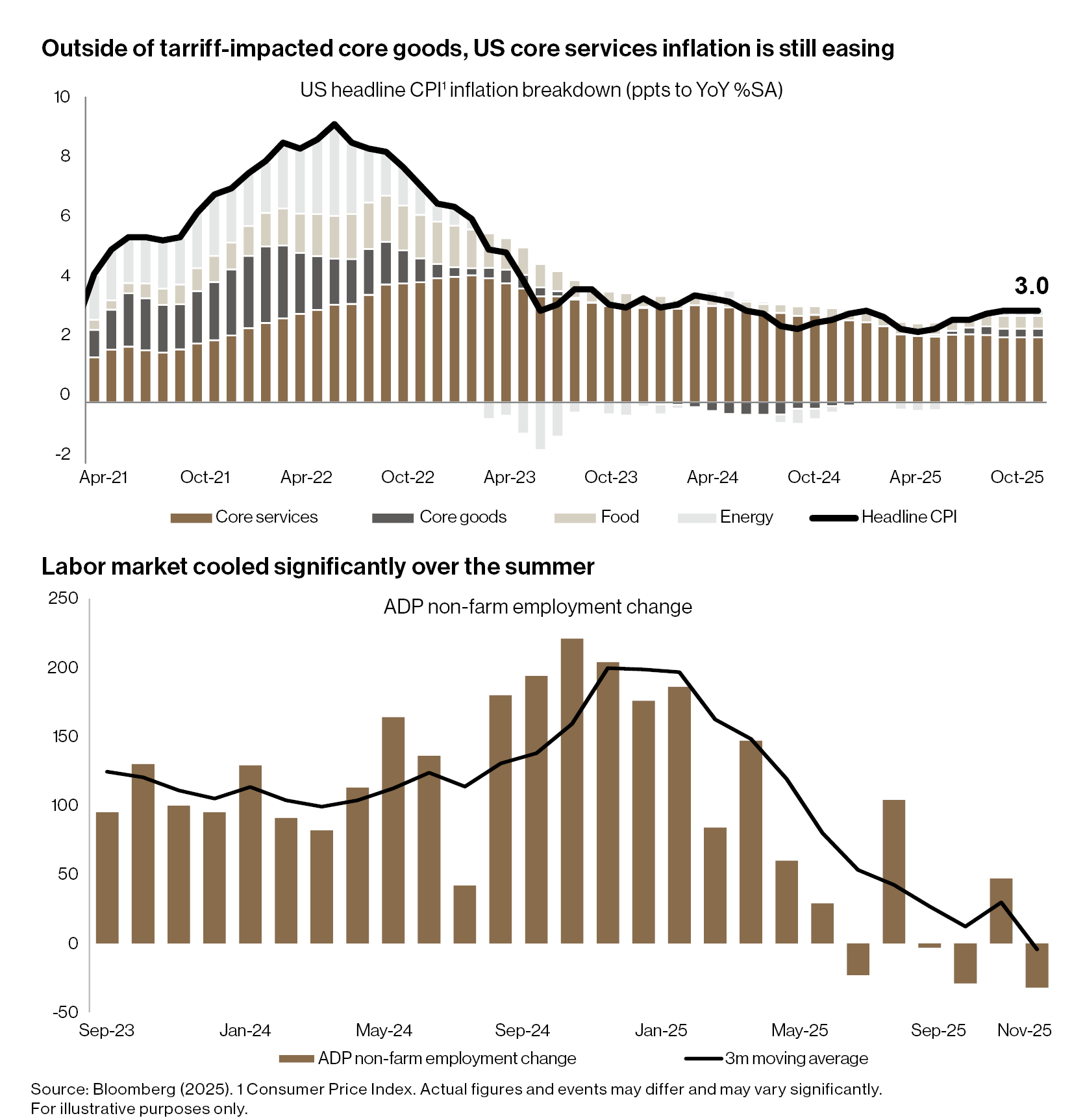

The US economy stands to benefit from recent Federal Reserve rate cuts, with additional easing likely in 2026 as labor market risks rise and inflation pressures diminish. Signs of strain are evident in layoffs across government, retail, and warehousing sectors, alongside a climbing unemployment rate and stalled job growth. Core services inflation is moderating, and tariff effects remain contained. With 75bps cuts delivered in 2025, we anticipate another 25-50bps in reductions in the year ahead.

Borrowing costs are already falling, creating some relief for households and corporates. Roughly USD 11 trillion in floating-rate debt1 is set to generate substantial interest savings, while tighter credit spreads and lower yields ahead of a large maturity wall in 2026–2027 should ease refinancing pressures for corporations. Together, these factors should support economic activity and employment.

Fiscal policy further reinforces this backdrop. The sweeping tax changes under the One Big Beautiful Bill Act (OBBBA) are anticipated to lift after-tax incomes by more than 5%2, creating tangible household savings. Accounting for additional measures aimed at corporates and businesses, these together represent roughly 1.2% of GDP growth. Midterm election dynamics could spur additional measures – such as tariff rollbacks or consumer-focused rebates – aimed at restoring consumer confidence.

Still, uncertainty remains a key consideration. A pending court decision on the tariffs imposed under the International Emergency Economic Powers Act (IEEPA), potential shifts in AI investment momentum, and the transition to a new Fed Chair could introduce volatility.

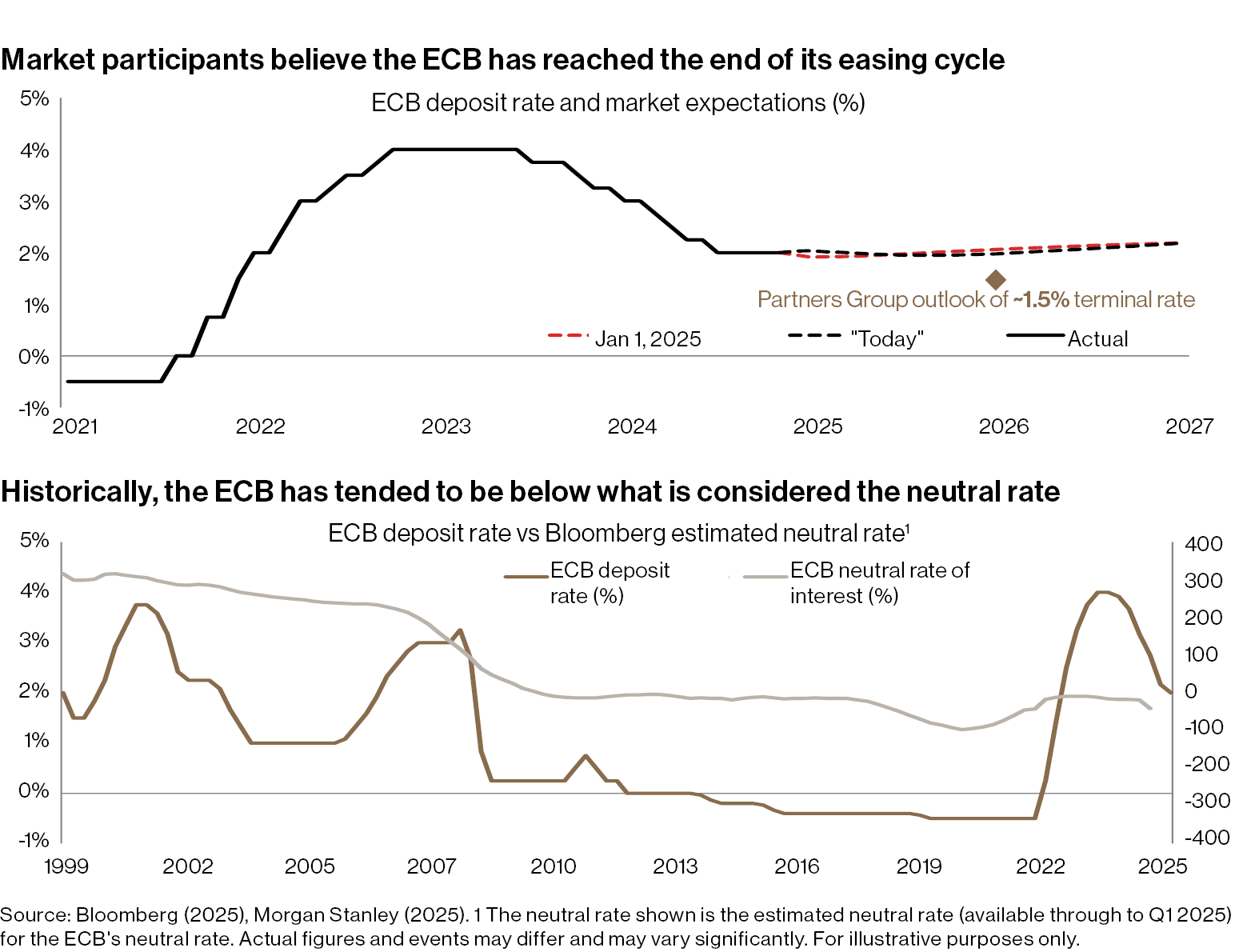

Europe: Mixed growth and muted inflation point to further ECB easing

Despite a pause, we anticipate the European Central Bank (ECB) to resume its easing cycle in 2026, likely delivering two 25bps cuts to reach a terminal rate near 1.5%. This is driven by persistent structural challenges in the Euro Area, where household-driven consumption remains weak.

Activity in early 2025 leaned on household and investment demand, but consumption continues to trail trend growth – particularly in Germany – underscoring the need for additional monetary support.

Encouragingly, household and corporate balance sheets are relatively healthy. However, wealth distribution remains highly uneven: the bottom half of households holds just 5% of total wealth and carries higher leverage, leaving them vulnerable to still elevated borrowing costs despite already implemented ECB easing.

External headwinds reinforce the case for rate cuts. Exports and industrial production are weakening as US demand normalizes and shipments to China slow, leaving Germany’s manufacturing sector particularly exposed to tariffs and global softness.

Inflation remains contained, supported by moderating wage growth, giving the ECB room to act. Fiscal policy is mixed across member states, but Germany’s pivot toward higher deficit spending offers support alongside the broader European push for defense spending. Together, these factors should help stabilize growth in the Euro Area.

China: Focus on consumption and reducing overcapacity

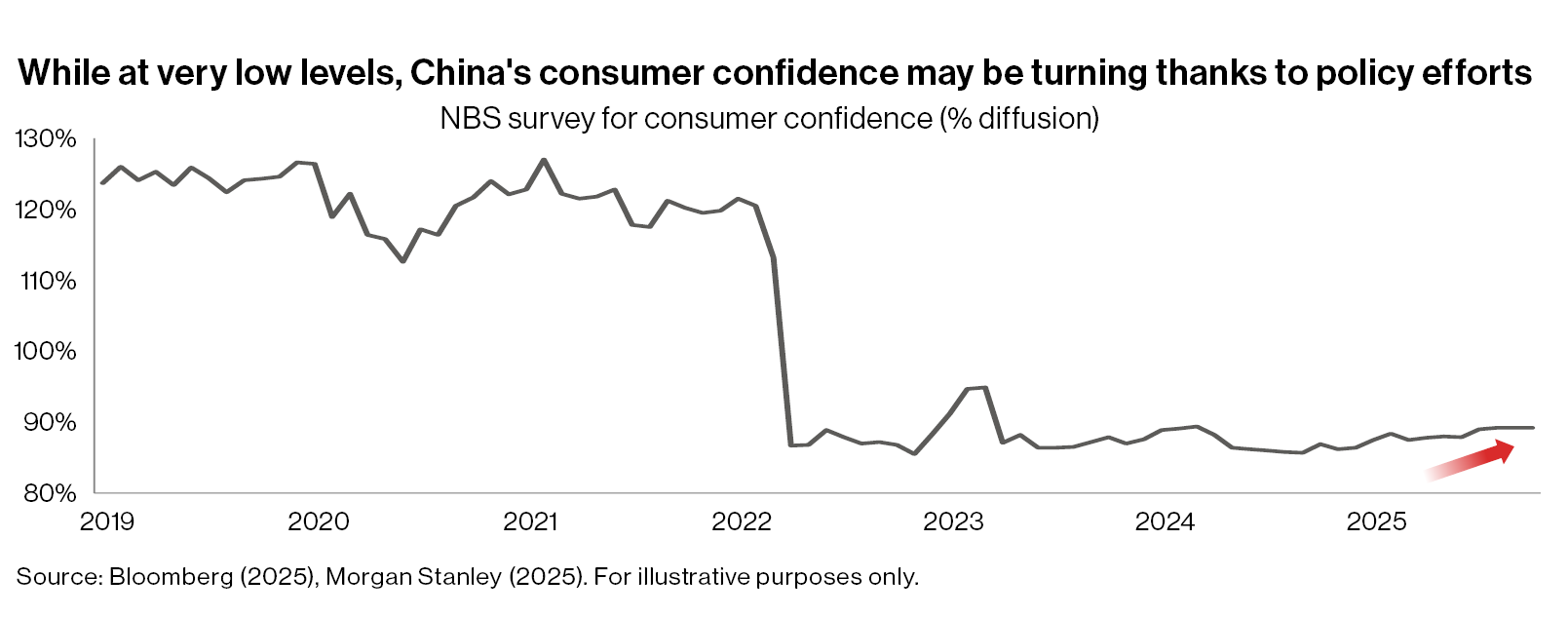

China’s fiscal stimulus, a key driver of resilience in recent quarters, appears to be losing momentum. Such policy measures have helped stabilize domestic activity, but their scale was modest and unlikely to deliver sustained growth. Deflation remains a major challenge, with two years of price declines driven by chronic overcapacity, adding pressure to household finances and corporate margins.

However, while consumer confidence remains historically low, recent government communication signals a stronger commitment to boosting household spending. At the same time, the government’s renewed campaign of "anti-involution"3 – targeting excess capacity across a broader range of industries – should restore balance over time, though near-term growth will be weighed down by capacity cuts and lower capex.

Looking ahead, Beijing’s roadmap combines tech selfreliance with structural efforts to promote domestic demand. Together with this, China's resilient exports and the recently agreed trade framework with the US provide a foundation for stability in 2026.

Five-Year Outlook: All Is Possible, More So Than Ever

The next five years will be shaped by multiple, often conflicting forces: from policy shifts and technological breakthroughs to demographic changes and geopolitical uncertainty. We frame our outlook as “All is Possible, More so Than Ever.” In this environment, investors should avoid hasty decisions and focus on what can be controlled: disciplined execution, scenario planning, and conviction in secular trends that endure across cycles.

Next, we outline key forces and how we expect to navigate them.

Artificial Intelligence: Opportunity, Productivity, and Disruption

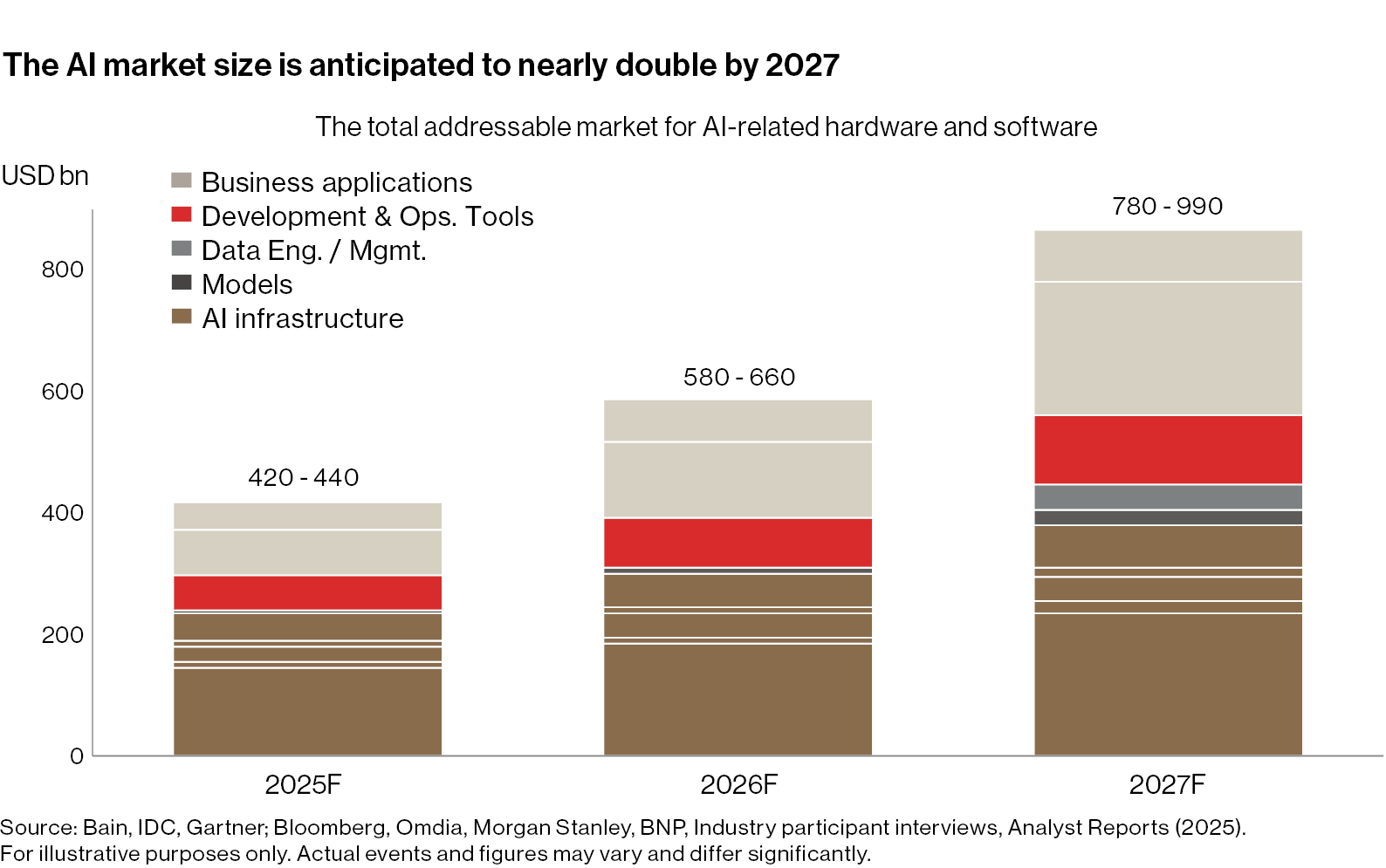

AI represents one of the most significant commercial opportunities for long-term investors. The total addressable market for Generative AI is projected to nearly double by 2027, approaching USD 1 trillion.

Despite concerns about rapid capex growth, demand trends and monetization signals remain strong: hyperscaler cloud revenues are accelerating, adoption rates are rising, and businesses report tangible productivity gains.

Our base case assumes continued adoption, though the “Electrification Moment” – where AI delivers broadbased productivity gains – may not arrive until after 2030. The trajectory will not be linear; setbacks are possible. Understanding AI-driven disruption is critical for investment decisions today, as it will define future winners and losers. Near-term beneficiaries include businesses with strong competitive moats and rapid integration capabilities. Longer-term winners will combine proprietary data with advanced AI tools or operate as AI-native disruptors.

Structural Upgrades: Infrastructure and Real Estate Modernization

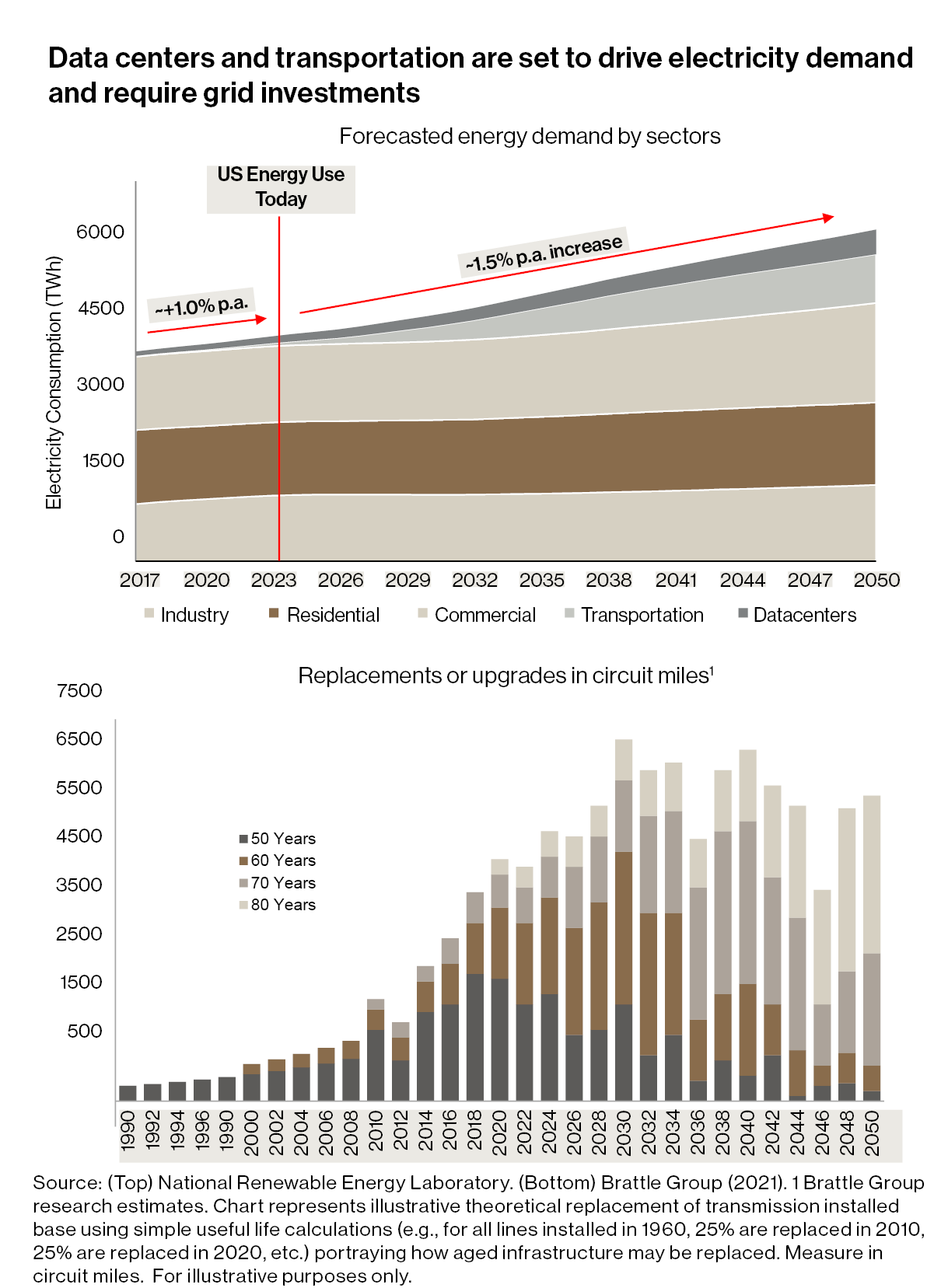

The global infrastructure landscape is entering a critical modernization phase after decades of underinvestment have left critical infrastructure and real estate assets outdated. Roads, bridges, electric grids, and water systems in advanced economies are operating beyond design life, while aging buildings lack the capacity for digital and energy-efficient upgrades. The American Society of Civil Engineers estimates that failing to upgrade these assets could cost the US economy USD 10 trillion in lost GDP by 2039, while McKinsey projects a staggering USD 106 trillion in global infrastructure investment will be needed through 2040.

AI adds urgency: data centers and power systems face surging demand, requiring trillions of dollars in investment for capacity, cooling, and grid resilience. This convergence of physical and digital infrastructure creates a defining investment theme for the next decade, spanning private equity, infrastructure, real estate, and private credit.

Discipline in data centres

Watch Esther Peiner, Global Head of Infrastructure, share our views on navigating capacity growth and market dynamics

Private Markets Implications

Both near-term dynamics and long-term structural forces shape our outlook for private markets. Our “Investing at High Altitude” macro view for 2026 anticipates increased activity in private equity and private credit. After several years of subdued investment and exit volumes, momentum has strengthened globally, with transaction activity rebounding sharply – a trend we expect to continue into 2026.

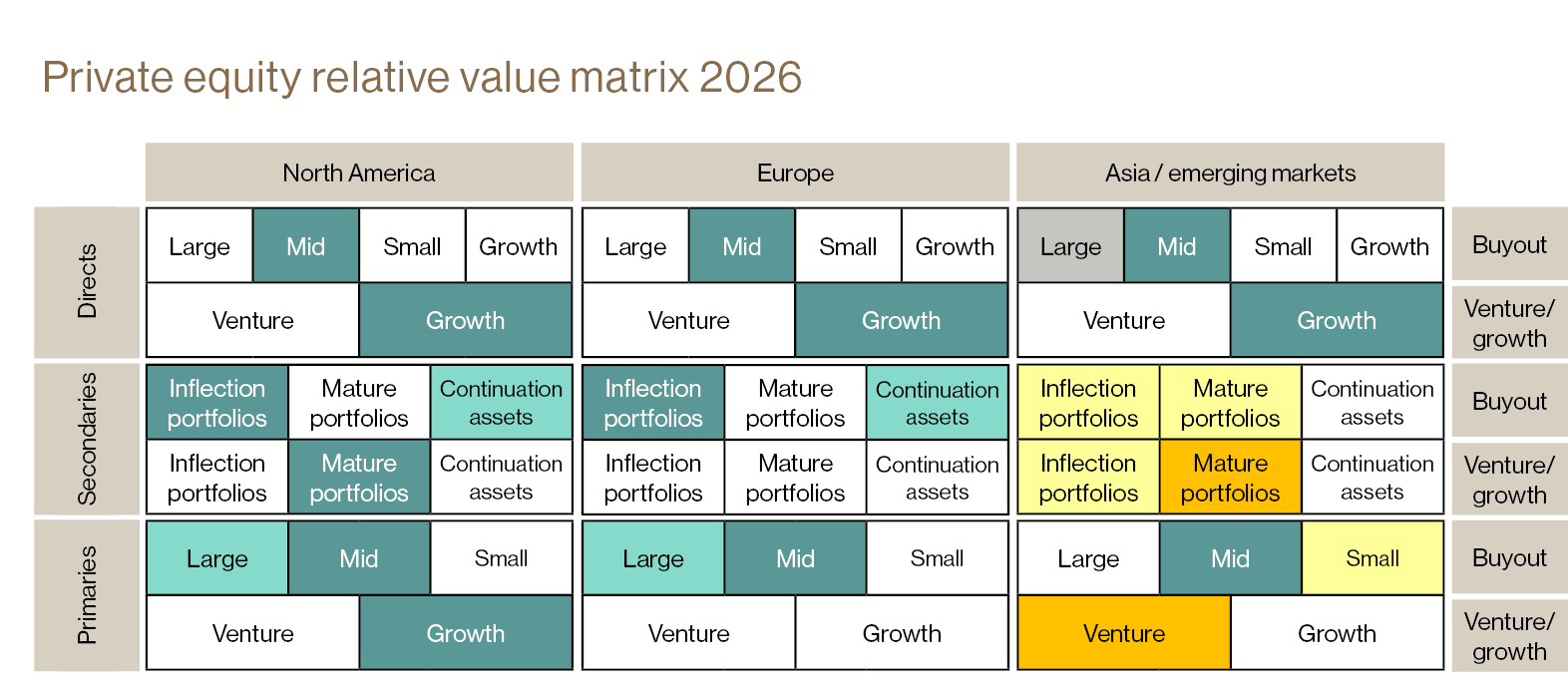

In the longer-term “All Is Possible, More So Than Ever” environment, we remain focused on performance resiliency through the cycles and adhere to our time tested investment approach. Given today’s valuation levels, identifying relative value across and within asset classes is critical.

Portfolio Construction Considerations

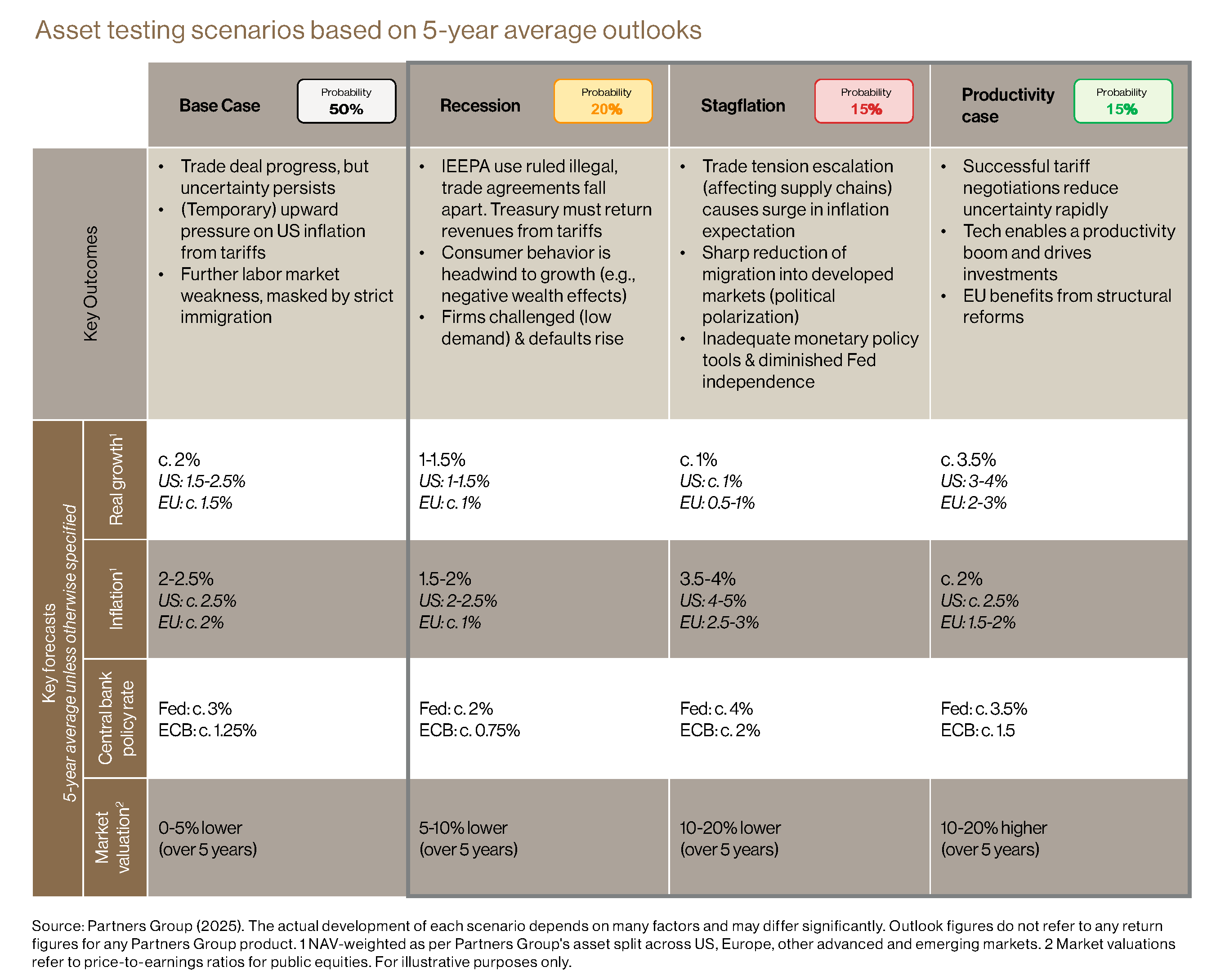

Stress-Test for Disruption – The complexity of near- and long-term outlooks underscores the importance of scenario analysis in underwriting. While our base case assumes continued growth and inflation normalization, we rigorously test for recession, stagflation, and productivity-boost scenarios.

Maintain Discipline in Thematic Investing – Despite recent market conditions supporting a more opportunistic approach, we continue to focus on long-term value creation through resilient structural themes. Our investments target assets driven by rising, structural demand rather than short-term economic cycles.

Build Portfolios Patiently – For private equity, we favor a 3-4-year build-up strategy to achieve vintage diversification. This approach provides flexibility to capitalize on volatility and valuation resets across our platform.

Ensure Regional Diversification – The US offers higher growth but carries inflation risk, while Europe presents lower entry valuations and cheaper credit against a backdrop of weaker consumption. We target balanced allocations: North America: 40-50%; Europe: 40-50%; and Rest of World: 10-20%.

Asset Class Outlooks

Private Equity

Attractive Flow, Selectivity Critical

Private equity is poised to benefit from a healthy flow of opportunities as transaction activity rebounds from several-year lows. Valuations have been moderating from their 2020-2021 peaks, while the macro backdrop has been supportive. We anticipate this momentum to continue into 2026, particularly in sectors such as pharmaceuticals and goods & products.

Our approach emphasizes control investments to actively steer companies through uncertainty, complemented by thematic investing in resilient structural trends. Opportunistic sourcing remains important to capture dislocations during periods of volatility.

In secondaries, we overweight inflection LP-led transactions given current discounts, while maintaining exposure to mature secondaries as competitors wind down older funds. GP-led continuation vehicles are growing in volume, but quality is uneven; we apply heightened scrutiny. Regionally, both the US and Europe present compelling opportunities.

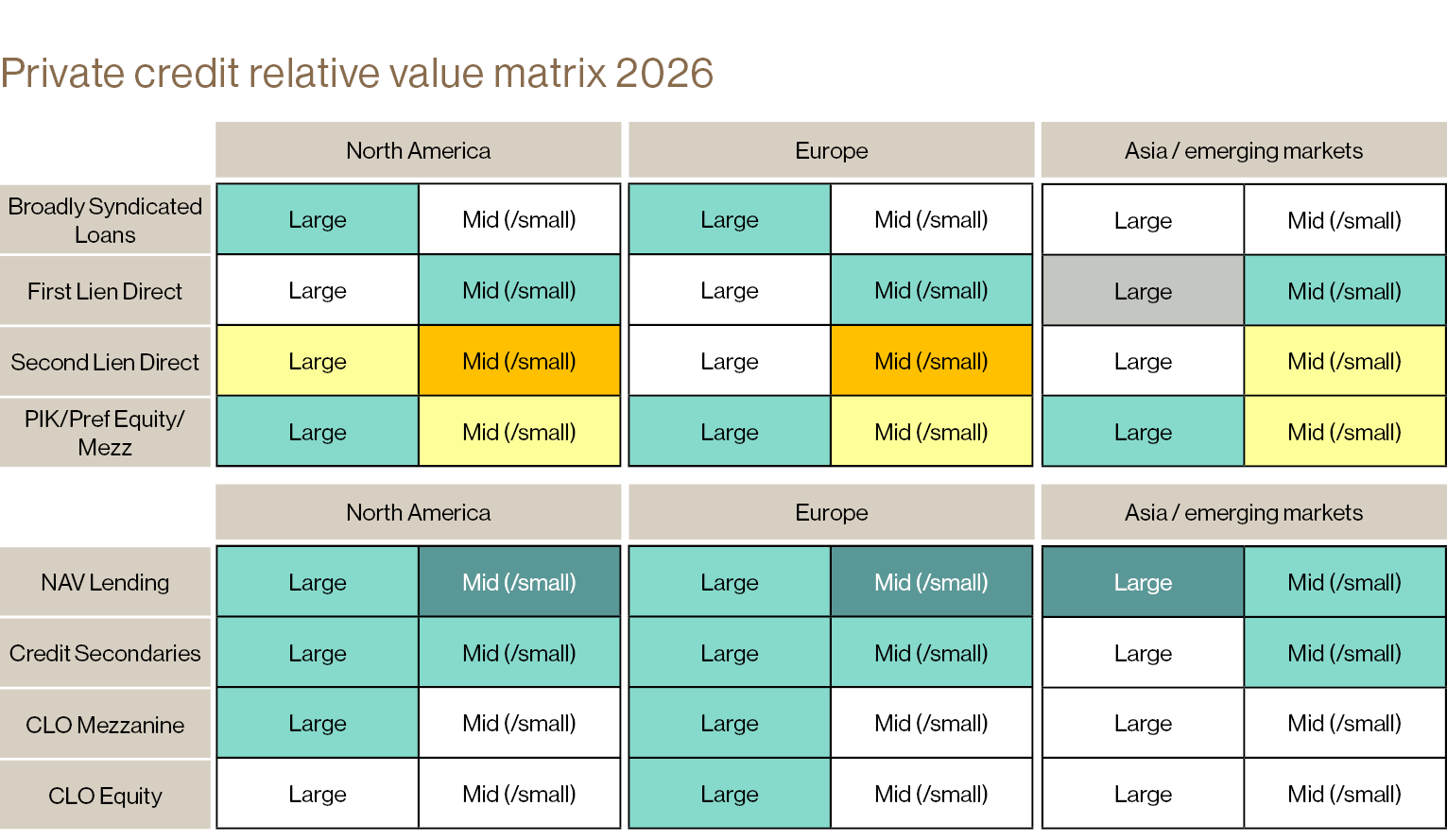

Private Credit

Resilient Profile Amid Moderating Returns

Private credit continues to present a compelling risk return profile despite some moderation in returns as global rate cuts lead to reduced base rates. While deployment and repayment activity remains healthy and steady, returns have moderated as base rates normalized. Overall credit quality remains stable, with leverage levels and default rates relatively low.

Relative value favors Europe over the US, thanks to wider spreads, lower leverage, and stronger creditor protections. We anticipate that bifurcation within the private credit market will intensify: direct lending to large companies may disappoint given margin compression and competitive pressures, whereas highly selective middle-market lending is expected to remain rewarding.

What's driving our private equity strategy

Watch video

Infrastructure investing beyond AI

Watch video

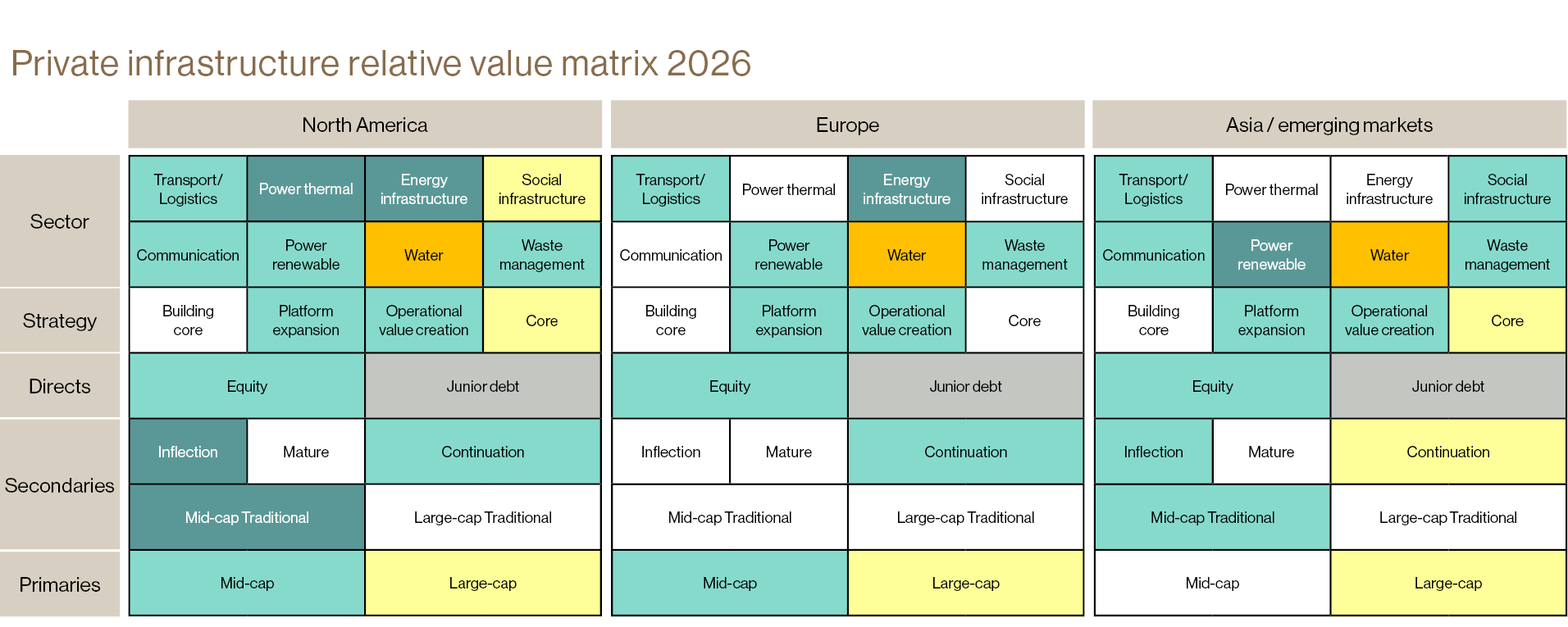

Infrastructure

Overweight for Resilience and Secular Growth

Infrastructure remains a strategic overweight in multi-asset portfolios, offering inflation-linked cash flows and resilience amid potential volatility. Secular trends – including AI-driven data center demand, power generation needs, and modernization cycles – reinforce the asset class’s long-term appeal. Direct infrastructure deployment is focused on selecting the right assets, while secondaries continue to provide stable and predictable flow. We favor mid-market inflection secondaries where discounts remain attractive.

Sector positioning is critical. Power and energy infrastructure in the US remains compelling, while Europe and Asia require selective approaches focused on business model viability beyond government support. It is important to note that additional due diligence may be required in certain sectors, such as renewables and data centers, to carefully assess regional demand and supply dynamics in light of policy changes, shifting priorities, and elevated valuations.

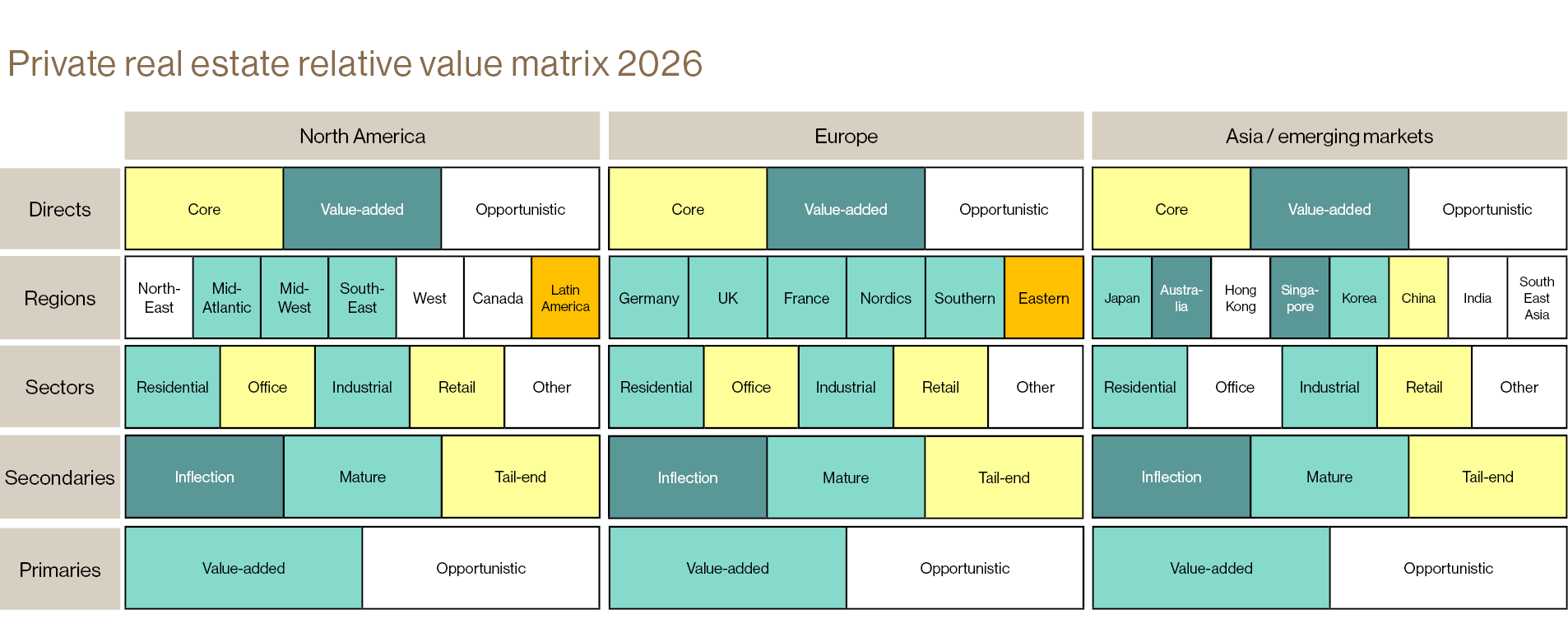

Real Estate

Value-Add Strategies and Regional Selectivity

Real estate investing requires a disciplined focus on value-add strategies, particularly in the US, where high interest rates relative to cap rates have made rent-driven returns challenging. While we anticipate lower interest rates will provide some relief, we maintain that sustainable returns must be anchored in operational value creation. In this context, the adoption of AI and technology continues to emerge as a critical value creation lever across real estate asset classes.

In the US, we maintain an overweight to Sunbelt markets, noting that recent oversupply is being gradually absorbed. In Europe, Southern markets are marginally more attractive than in prior cycles, positioning us as both buyers and sellers depending on market conditions. In Asia-Pacific, Australia and Singapore remain preferred despite competitive bidding from local capital. Across regions, we continue to prioritize residential and industrial assets, closely monitoring local supply-demand imbalances and trends in rental growth. With direct transaction activity remaining muted globally, we see attractive opportunities in secondaries, where good discounts to fair market value can be found.

The expanding opportunity set in royalties

Watch video

Royalties

Expanding Market and Portfolio Diversification

We anticipate royalty investing to continue to gain traction as a portfolio diversifier, offering low correlation and resilience through market volatility. The royalty market is estimated at USD 2 trillion and continues to grow. While established sectors such as pharmaceuticals, energy, music and broader entertainment remain core, new areas like sports and technology are emerging, further expanding the opportunity set. (Read our Royalties primer for more.)

For companies looking at funding sources, royalty financing offers a non-dilutive alternative to equity and, unlike traditional credit, does not require debt capacity, making it particularly attractive for businesses seeking flexible capital solutions. 2025 was a pivotal year for Partners Group, marked by the launch of the world’s first cross-sector royalty offering through evergreen structures. Looking ahead to 2026, we anticipate continued expansion of royalty structures and increased lending against royalties.

Staying Grounded at High Altitude

As we enter 2026, private markets face a landscape defined by elevated valuations across markets, policy shifts, and transformative secular trends. While the current environment offers the potential for further progress, it also brings the risk of setbacks from these heights. Maintaining discipline – through rigorous valuation, scenario analysis, and a focus on long-term value creation – remains essential. By staying grounded and attentive to both opportunities and risks, we are positioned to capture value for our clients, regardless of how the terrain evolves.

Discover more

Partners Group's recent thought leadership

Private Markets Chartbook Q4 2025 Unlocking Europe’s Living OpportunityAuthors