With the Strait of Hormuz gradually reopening between mid-June and mid-July, oil prices have moved materially lower, retracing a significant portion of their conflict-driven spike. Looking ahead, while current developments suggest that further normalization remains in flux, markets must come to grips with a key reality: a swift or permanent restoration of the pre-war status quo in the Middle East is unlikely in the immediate future. Accordingly, we do not expect oil prices to revisit their conflict highs, nor do we see them fully retracing to pre-conflict levels. Rather, we expect crude to retain a modest premium, reflecting both the scale of the realized inventory drawdown and lingering uncertainty around the durability of any further ceasefire agreements. Even so, the path forward now points to Brent in the mid- to high-USD 70s per barrel by year-end 2026 – well below the levels we were modeling prior to the mid-June ceasefire, yet still above pre-conflict levels1.

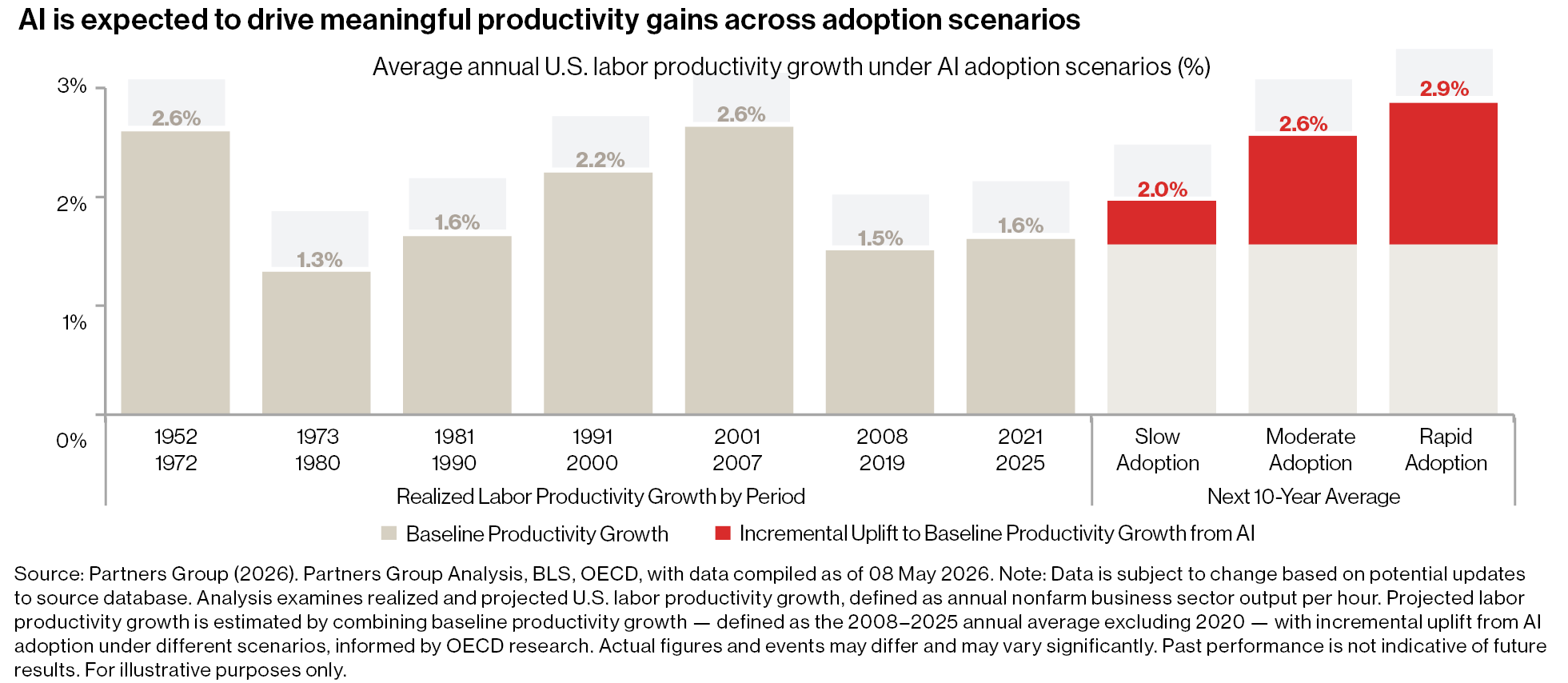

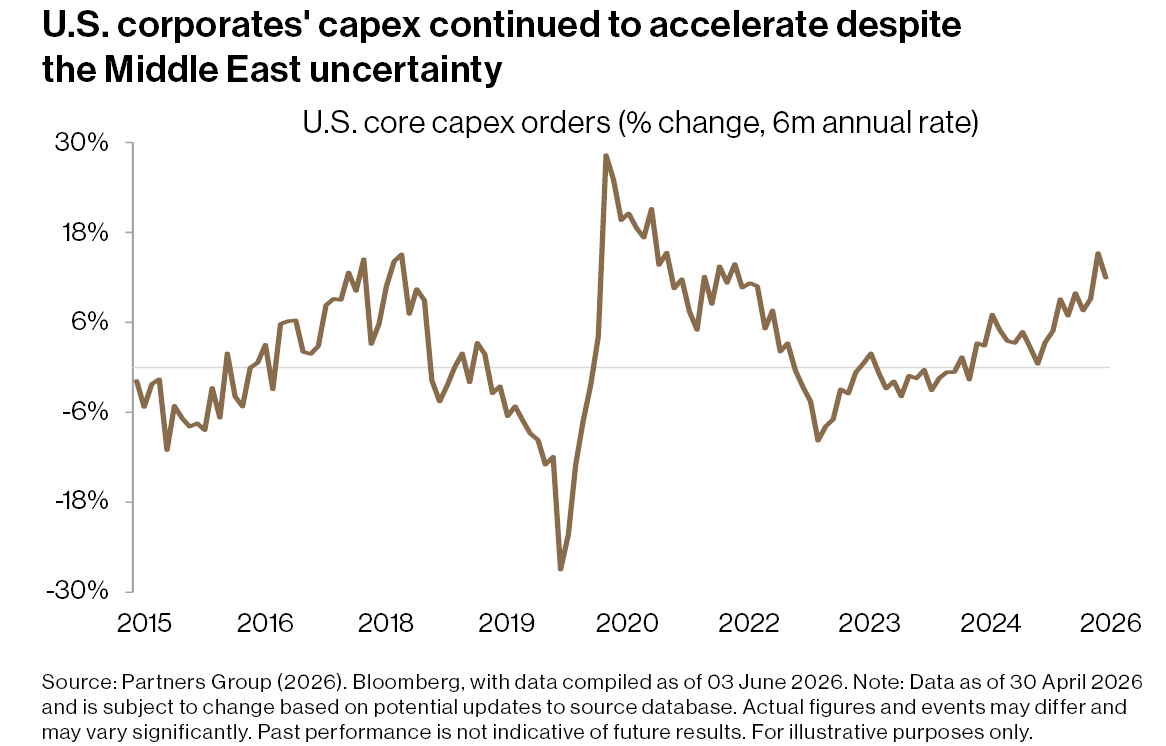

The change in oil prices has materially improved the growth backdrop, transforming what had been shaping up to be a sustained drag on growth into an environment where the economy can refocus on its three core engines: resilient U.S. consumption, durable corporate profitability, and a powerful capex impulse. Consumer growth continues at a fair clip in the U.S., supported by real income gains as energy-cost increases fade. Corporate profitability remains resilient, particularly in the U.S. And the emerging dominant story is capital expenditure.

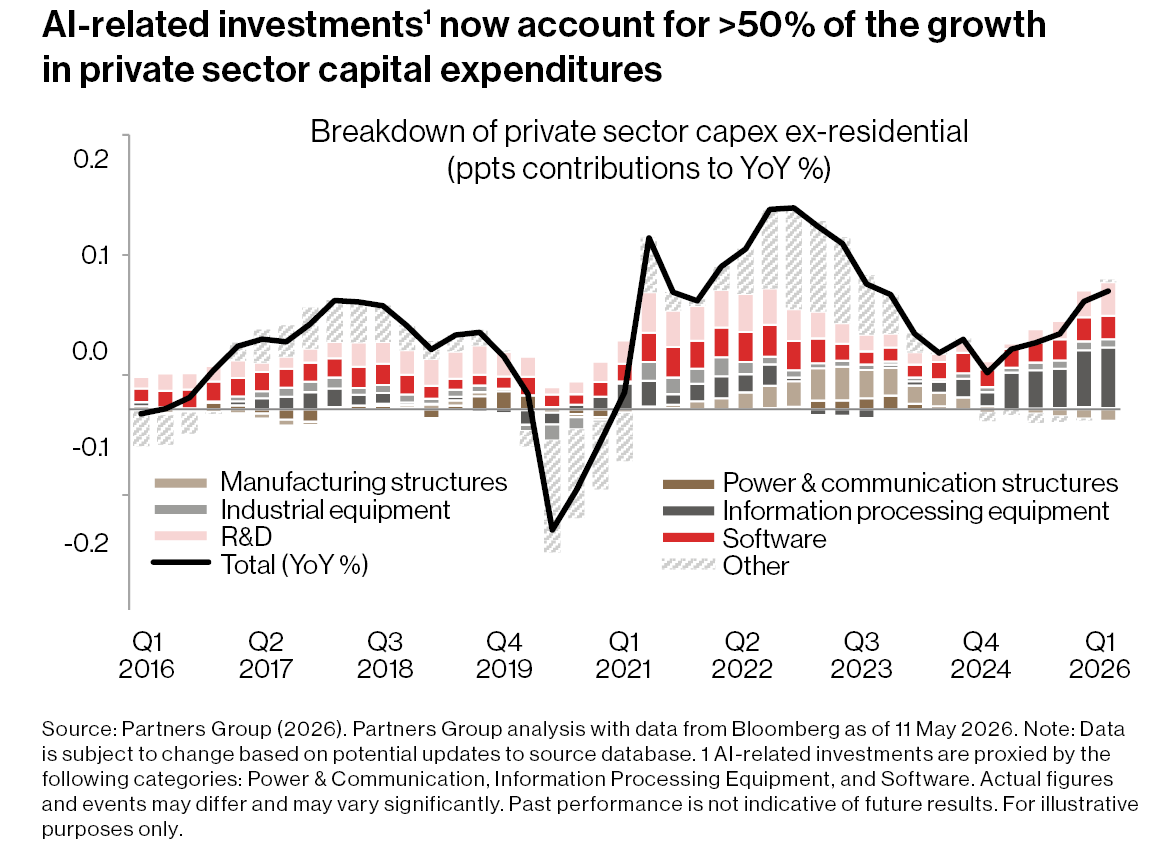

In the U.S., AI-related investment now accounts for more than half of the growth in private-sector capex2, propelling core capex orders to their fastest pace since the post-COVID period3. In Europe, defense procurement plays an equivalent role: military spending is on track for a sharp acceleration in 2026, with the vast majority of procurement now flowing to European contractors rather than U.S. suppliers – a meaningful boost to domestic activity.

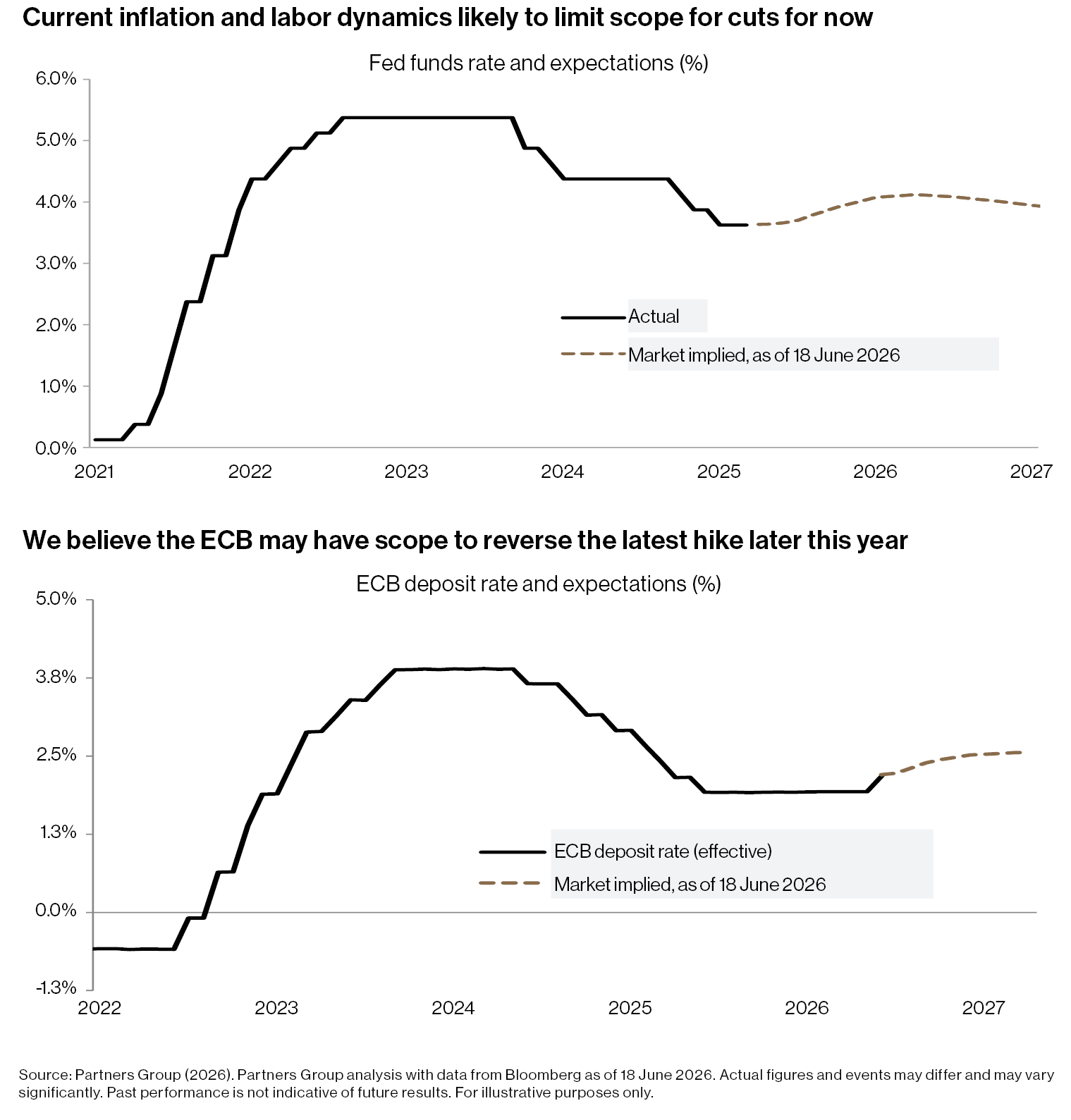

The monetary policy backdrop has eased in parallel. With energy prices retreating and second-round effects on inflation appearing largely limited across economies, we see scope for major central banks to adopt a more dovish posture than appeared likely at the height of the conflict.

In the U.S., we continue to view the Federal Reserve as biased dovishly, with rates on hold for now, but cuts remain a possibility later in 2026 – especially as core CPI is appearing to have neared its peak4. In Europe, while the ECB delivered a hike in June, anchored long-term inflation expectations and a less tight labor market argue against further monetary policy tightening – and we see scope for that hike to be reversed in the second half, provided the energy backdrop doesn't change. In such a scenario, we see a constructive near-term base case assuming the U.S.-Iran agreement holds.

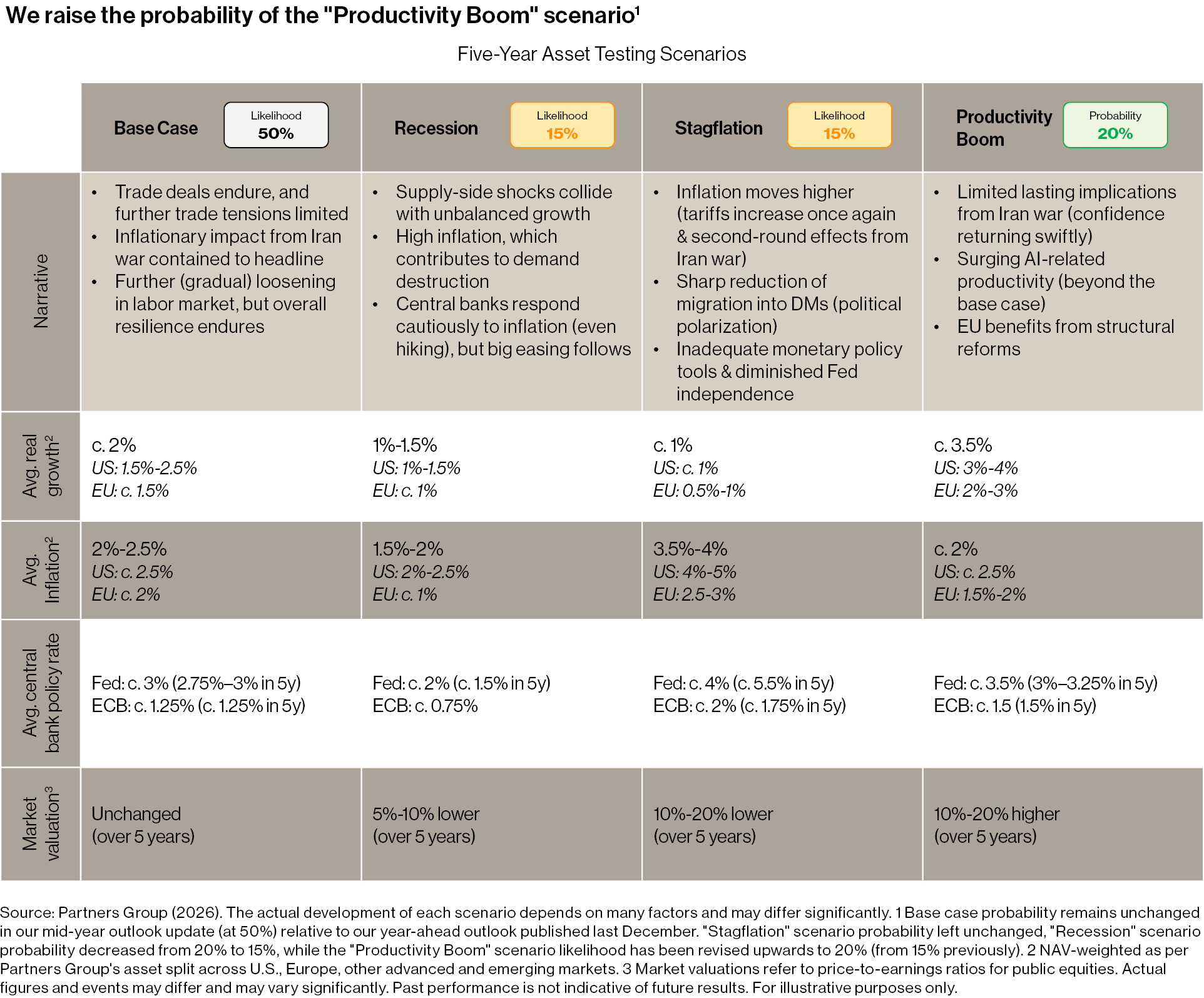

Base Case: A Constructive Re-Acceleration

Under our base case, oil settles at a modest premium to pre-war levels through the second half of the year as inventories are gradually rebuilt5. The drag from the Iran conflict largely fades, allowing growth to revert to – or modestly exceed – its pre-war trajectory.

Regionally, the U.S. remains the relative outperformer, with growth in the 2.5-3.0% range supported by AI-related investment, resilient consumption, and fiscal support from the One Big Beautiful Bill Act. Europe expands at 1.5-2.0%, with German fiscal expansion and the defense spending surge offsetting still-fragile consumer demand. China remains stable, supported by strategic energy reserves, a diversified energy mix, and ongoing policy flexibility.

Headline inflation moderates as energy prices ease, with U.S. CPI converging towards 2.5% and the Eurozone closer to 2% by year-end6. Core inflation in both regions runs near target, giving central banks scope to hold – or, in the U.S. case, to begin cutting later in the year.

Financing conditions remain supportive: borrowing costs have already retraced meaningfully from their peak, and a stable-to-lower rate path should support refinancing activity and new transaction underwriting through the second half. That said, sponsors are likely to maintain underwriting discipline given how recently the macro picture shifted.

Risk Monitor: A Fragile Agreement

The downside risk has not disappeared. The U.S.-Iran ceasefire remains fragile, and the path back to a sharper supply-side shock is short: renewed conflict, infrastructure damage in the Gulf, or extended disruption to flows through the Strait of Hormuz would all reintroduce stress quickly.

Under that scenario, oil could move back towards the May 2026 highs, potentially adding 50-100 bps to headline inflation and shaving up to a full percentage point off Eurozone growth7. Recent developments have made this risk more prominent than it was at the time of the signing, but a full unravelling – with sustained closure of the Strait of Hormuz and a return to the peak-conflict energy shock – is not our central view.